Publication

La Cour suprême du Canada tranche : les cadres ne pourront se syndiquer au Québec

Le 19 avril dernier, la Cour suprême du Canada a rendu une décision fort attendue en matière de syndicalisation des cadres.

Mondial | Publication | September 2014

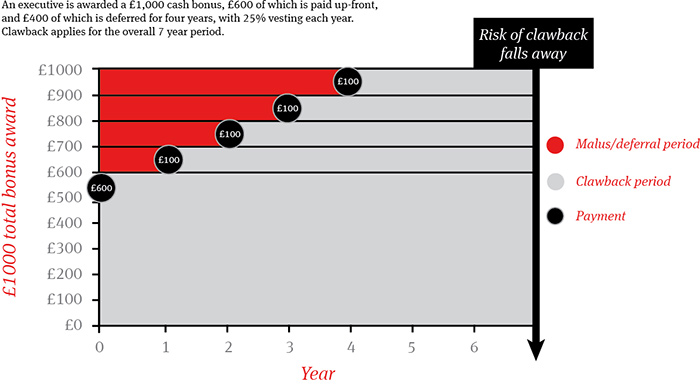

On 30 July 2014, the PRA published a policy statement (PS7/14) announcing the revised clawback obligations which will apply to PRA-regulated firms in remuneration levels one and two following the earlier clawback consultation paper published in March 2014 (CP6/14). The changes come as regulators in both the UK and Europe focus on the rights of banks to require repayment of bonuses in the light of a number high-profile controversies.

Following the amendments to the PRA Remuneration Code which is currently set out in Chapter 19A of the FCA’s Systems and Controls Handbook, all variable remuneration (both short and long-term, cash and non-cash) awarded to material risk takers on or after 1 January 2015 must be subject to ex-post risk adjustment through combined malus and clawback provisions:

The particular circumstances in which firms are required to provide for clawback are where:

Following the consultation, the PRA have recognised the need to limit requirements to pay back remuneration to serious individual misconduct and risk failure, whereas the wider malus provisions are triggered where the firm or relevant business unit suffers a material downturn in its financial performance (without individual culpability), as well as for individual misconduct and risk failure as set out above. The revised rule requires firms to “make all reasonable efforts” to recover an appropriate amount, with the policy statement acknowledging that firms are able to take a proportionate approach based on the assessment of individual cases. This addresses concerns expressed by respondents to the original consultation about the difficulties of seeking recovery where an individual is resident in a jurisdiction in which clawback is not enforceable.

Whilst some elements of the new requirements are clear and the clarifications on measuring the clawback period from the date of award (rather than vesting) are welcome, in establishing their clawback policies firms should consider their approach to the following questions:

The policy statement does not require that behaviour leading to clawback should be the subject of regulatory investigation or sanction and as such, the focus is on a firm’s internal investigations and determinations. In addition, whilst the policy statement makes it clear that the PRA believe clawback is most appropriate in circumstances involving individual culpability, it may be difficult in practice to distinguish between an individual’s misbehaviour and an organisational cultural failure.

For example, where instruments have been awarded, should it be the value of the instruments at the time of award, or at a later date such as vesting or when the clawback provisions are triggered? And should amounts be recouped on a gross or net of tax basis? Firms will need to ensure that the relevant documentation specifies how the requisite amount is to be determined.

Given that firms may need to clawback amounts which were paid several years previously and are likely to have been converted into cash and spent, it is vital to ensure that clawback provisions are both enforceable and operable in practice. Whilst the simplest approach would be to require all variable remuneration to be held by a nominee or in escrow until the clawback period expires, this would understandably be unacceptable to most executives, therefore, firms should ensure that:

It nevertheless may be particularly difficult to enforce recoupment from an individual once they have left and in these circumstances firms may wish to consider whether it would be desirable to require departing executives to place any money or share awards in escrow until the clawback rights fall away.

As well as the new clawback provisions, the PRA and FCA have also announced a number of proposals designed to further strengthen the alignment of risk and reward, including:

The proposed categorisation of senior managers for these purposes is set out further in PRA CP14/14.

If you have any questions about clawback and/or the other PRA and FCA proposals relating to variable remuneration, please contact one of the Norton Rose Fulbright team featured at the top of this briefing.

Publication

Le 19 avril dernier, la Cour suprême du Canada a rendu une décision fort attendue en matière de syndicalisation des cadres.

Publication

Le budget 2024 propose d’élargir la portée de certains pouvoirs permettant à l’ARC de demander des renseignements aux contribuables tout en prévoyant de nouvelles conséquences pour les contribuables contrevenants.

Publication

L'impôt minimum de remplacement (IMR) est un impôt sur le revenu additionnel prévu dans la Loi de l’impôt sur le revenu (Canada) (la « Loi ») auquel sont assujettis les particuliers et certaines fiducies qui pourraient autrement avoir recours à certaines déductions et exemptions et à certains crédits pour réduire leur impôt sur le revenu fédéral canadien régulier.

Abonnez-vous et restez à l’affût des nouvelles juridiques, informations et événements les plus récents...

© Norton Rose Fulbright LLP 2023